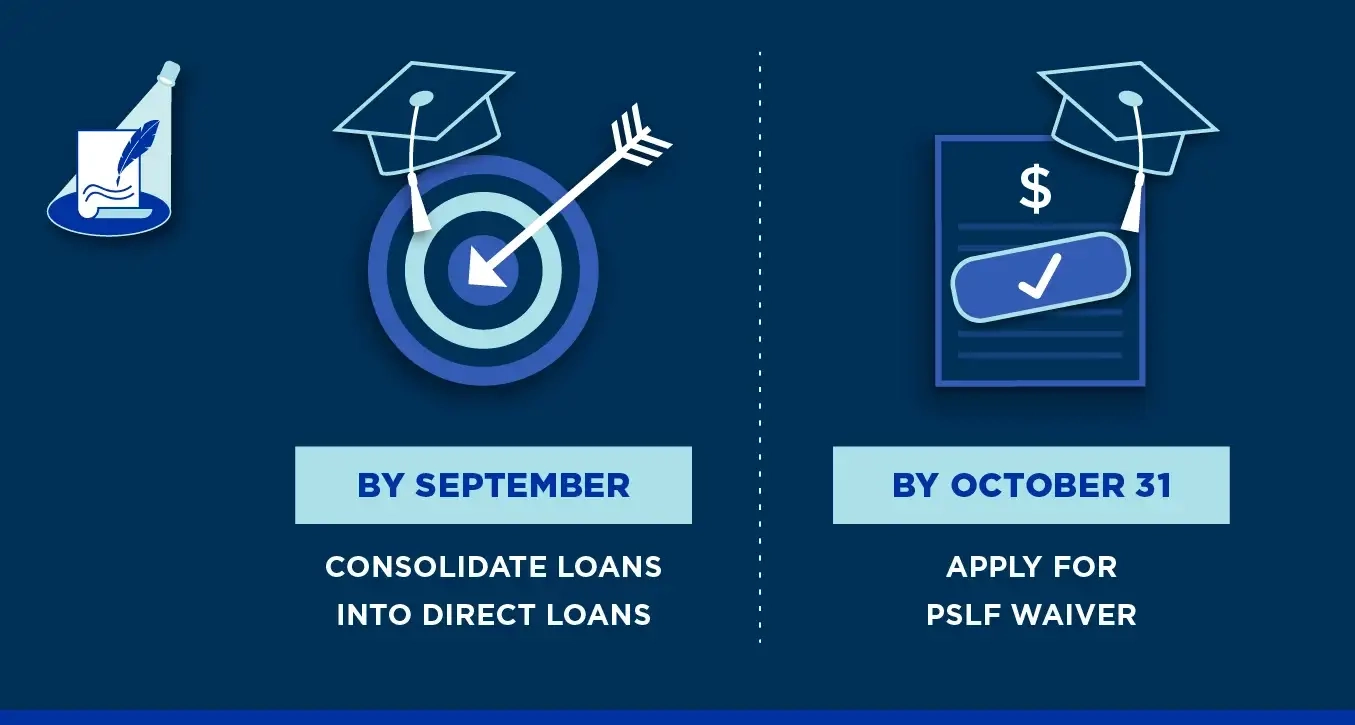

Some eligible borrowers must first consolidate their loans into Direct Loans, which can take 45+ days, before filing a waiver application, so the time to act is now!

Confusion reigns regarding the Biden administration’s student loan forgiveness initiative–who qualifies, which loans are eligible, what borrowers need to do–announced at the end of August. Borrowers with questions should go to www.studentaid.gov/debt-relief-announcement/.

The initiative plans to erase $10,000 in debt for borrowers making less than $125,000 and $20,000 for those who received Pell grants. It is likely to face legal challenges: “It is incumbent upon the advocates and policymakers who pushed to take this unprecedented step to also communicate to borrowers that there is a strong chance it will never come to fruition,” says Lanae Erickson, senior vice president for social policy, education and politics at The Third Way, a center-left policy think tank, in the New York Times.

Complicating matters further is an upcoming October 31 deadline to apply for what’s called the limited Public Service Loan Forgiveness Waiver for which employees of nonprofits and governments are eligible, generally. Yet only 15 percent of eligible borrowers have applied, estimates the Student Borrower Protection Center.

Compounding the PSLF complication: many borrowers who are eligible for the waiver must first convert their loans into Direct Loans ahead of the deadline before they can apply, a process that can take up to 45 days — so the time for eligible borrowers to act is now!

Given the connections among student loan debt, mental health, stress, employee wellness and productivity, government and nonprofit employers can help themselves and their employees by making employees aware of the limited PSLF waiver deadline. In 2021, more than 30,000 borrowers eliminated an average of nearly $67,000 through the waiver.

As a resource for employers, we put together an easily shareable Q&A for employees on everything borrowers need to know to apply.

What is PSLF?

If you are employed by a U.S. federal, state, local, or tribal government or not-for-profit organization, you may be eligible for the Public Service Loan Forgiveness Program. The PSLF Program forgives the remaining balance on your Direct Loans after you have made 120 qualifying monthly payments under a qualifying repayment plan while working full-time for a qualifying employer.

What is the “limited PSLF waiver?”

Last fall the U.S. Department of Education (ED) announced a change to Public Service Loan Forgiveness (PSLF) program rules for a limited time as a result of the COVID-19 emergency. Borrowers may receive credit for past periods of repayment that would otherwise not qualify for PSLF by applying for the limited PSLF waiver by October 31, 2022.

Am I eligible for PSLF and the limited PSLF waiver?

The best way to know if you’re eligible is to apply today using the PSLF Waiver Help Tool.

You don’t have to use the Help Tool to generate a PSLF form with your employer, BUT your form will be processed more quickly if you do, so it’s best to use it.

To qualify for PSLF, generally, you must meet the following criteria:

- be employed by a U.S. federal, state, local, or tribal government or not-for-profit organization (federal service includes U.S. military service);

- work full-time for that agency or organization;

- have Direct Loans (or consolidate other federal student loans into a Direct Loan);

- repay your loans under an income-driven repayment plan (This provision is waived through October 31, 2022 as part of the limited PSLF waiver.);

- make 120 qualifying payments.

Search here to see if your employer qualifies. And, if you’re a public service worker in New York City, then check out PSLF.nyc, a nonprofit effort working with nonprofits, unions, and government agencies to help 250,000 public service workers in NYC get their loans forgiven.

Which loans qualify for PSLF and the waiver?

Any loan received under the William D. Ford Federal Direct Loan (Direct Loan) Program qualifies for PSLF.

Loans from the Federal Family Education Loan (FFEL) Program and the Federal Perkins Loan (Perkins Loan) Program don’t qualify for PSLF. However, they may become eligible if you consolidate them into a Direct Consolidation Loan.

“Borrowers who currently have FFEL, Perkins, or other non-Direct Loans, will get the benefit of this limited waiver if they apply to consolidate into the Direct Loan program and submit a PSLF form by October 31, 2022” — but the consolidation process can take 45 days, so borrowers should act now.

The waiver enables eligible “student borrowers to count all payments made on loans from the Federal Family Education Loan (FFEL) Program or Perkins Loan Program,” including ones that didn’t previously count.

How do I consolidate my non-Direct Loans?

Go here to consolidate qualifying federal student loans including outstanding FFEL and Perkins loans into a Direct Loan, to take advantage of the limited PSLF waiver. It’s free to apply. Be aware that private companies may offer to help you consolidate your loans for a fee, but it’s free to apply. Knowledge is power, and in this case money.

How does the federal student loan payment moratorium impact my PSLF eligibility?

The Biden administration announced that it is extending the current moratorium on payments until Dec. 31 and implementing a new cap on the maximum monthly payments of undergraduate borrowers, among other changes.

Under the moratorium, each month since it began counts as a qualifying loan payment. If you paused your payments for the past 26 months, then you registered 26 on-time payments, bringing you 26 payments closer to your goal of 120 qualifying payments toward forgiveness.