What You Need to Know about the CARES Act

Brief Overview

The CARES Act is a $2 trillion emergency package signed into law on March 27, 2020 with the intention of mitigating the economic impact of the coronavirus pandemic.(1) Click here to view Spanish version.

It includes:

- One time direct payments to citizens who filed income tax returns in 2018 or 2019, who could not be claimed as a dependent of another taxpayer, and with adjusted gross income under certain limits(1)

- One time direct payments to non-citizens living and working in the US with a valid Social Security Number who filed income tax returns in 2018 or 2019, who could not be claimed as a dependent of another taxpayer, and with adjusted gross income under certain limits(1)

- One time direct payment to non-filers who are citizens or non-citizens with a valid Social Security Number that meet the substantial presence test. Non-filers include those who in 2018 and 2019 had gross income that did not exceed $12,200 ($24,200 for married couples). It also includes those who aren’t typically required to file taxes (such as Social Security beneficiaries, survivor beneficiaries, Railroad retirees, SSI, SSDI)

- An increase in the amount and an expansion of the eligibility of unemployment benefits(2)

- Loans (which can be partially or entirely forgiven depending on eligibility) for small businesses and non-profits(3)

- Free counseling and low-cost training for small businesses(3)

- Temporary pause on student loan payments and interest

06/19/20

Common Questions

One Time Direct Payments

Student Loans

Unemployment

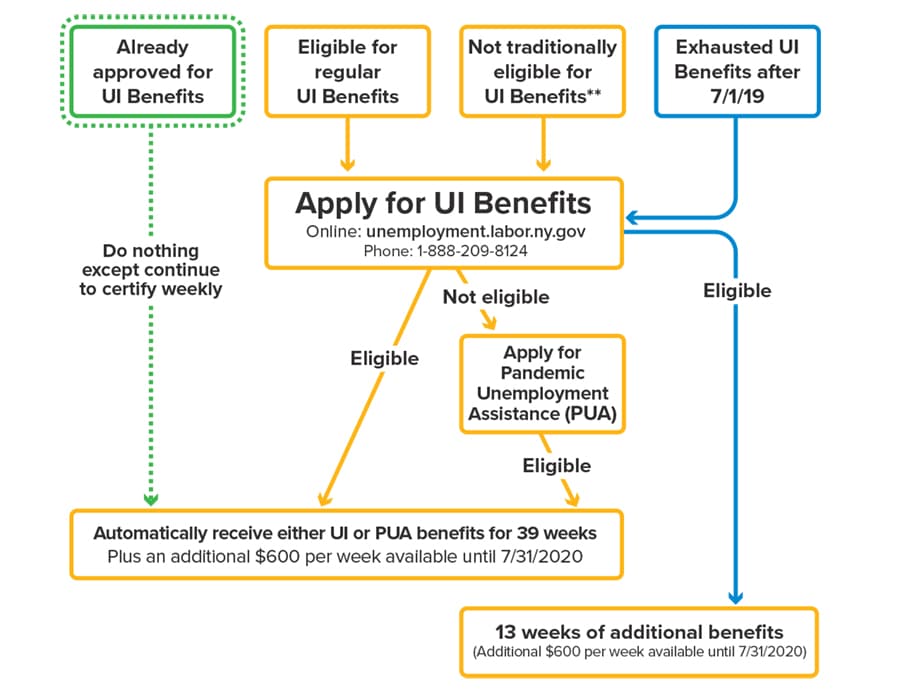

- Unemployment benefits have been extended from 26 to 39 weeks.

- In addition to one’s usual unemployment benefit, recipients will receive an additional $600/week starting 4/5/20 through 7/31/2020.(7)

- Eligibility has been expanded but one still applies through the regular state-specific channels(e.g. NY Dept of Labor)

- Pandemic Unemployment Assistance (PUA) provides emergency support for workers who are left out of their state’s standard unemployment coverage, workers who have already exhausted those benefits or workers who are unable to work due to certain circumstances caused by the coronavirus pandemic.(6)

- According to the National Employment Law Project (NELP), those eligible for PUA include: self-employed workers, independent contractors, freelancers, workers seeking part-time work, workers who do not have a long-enough work history to qualify for state UI benefits, and workers who have exhausted their standard state UI benefits. Importantly, those who are eligible for their state’s normal unemployment benefits do not qualify for this special pandemic assistance.

- You have been diagnosed with COVID-19 or have symptoms of it and are seeking diagnosis

- A member of your household has been diagnosed with COVID-19

- You are providing care for someone diagnosed with COVID-19

- You are providing care for a child or other household member who can’t attend school or work because it is closed due to COVID-19

- You are quarantined or have been advised by a health care provider to self-quarantine

- You were scheduled to start employment and do not have a job or cannot reach your place of employment as a result of a COVID-19 outbreak

- You have become the breadwinner for a household because the head of household has died as a direct result of COVID-19

- You had to quit your job as a direct result of COVID-19

- Your place of employment is closed as a direct result of COVID-19(6)

- The PUA program runs from January 27, 2020 through December 31, 2020, and benefits can be received retroactively for qualifying applicants. Eligibility ends on December 31, unless the program is later extended.

- PUA benefits can be claimed for a maximum of 39 weeks.(6)

- The calculations are based on the federal Disaster Unemployment Assistance program under the Stafford Act, which means the minimum weekly benefit amount payable is half (50%) of the average benefit amount in the state you apply in. According to the NELP, that’s about $190 per week.(6)

- Begin by visiting your state’s labor department or equivalent website. For New Yorkers, head to labor.ny.gov. If you are not traditionally eligible for unemployment benefits, begin the standard unemployment insurance application process, and apply for Pandemic Unemployment Assistance.(6)

- No. Workers must be authorized to work to be eligible for the program.

- Yes. If you qualify for PUA but do not traditionally qualify for your state’s unemployment insurance, you also qualify for:

- The Pandemic Unemployment Compensation (PUC): An additional $600 per week through July 31, 2020, and;

- Pandemic Emergency Unemployment Compensation (PEUC): An extended 13 weeks of coverage provided to unemployed individuals who have exhausted

Self-Employed/Small Business

Retirement Accounts

- https://www.nbcnews.com/politics/congress/coronavirus-checks-direct-deposits-are-coming-here-s-everything-you-n1168936

- https://www.nbcnews.com/politics/congress/coronavirus-unemployment-benefits-here-s-who-qualifies-how-much-they-n1169846

- https://www.sbc.senate.gov/public/_cache/files/2/9/29fc1ae7-879a-4de0-97d5-ab0a0cb558c8/1BC9E5AB74965E686FC6EBC019EC358F.the-small-business-owner-s-guide-to-the-cares-act-final-.pdf

- https://www.irs.gov/newsroom/economic-impact-payments-what-you-need-to-know

- https://www.nbcnews.com/politics/congress/coronavirus-checks-direct-deposits-are-coming-here-s-everything-you-n1168936

- https://www.syracuse.com/coronavirus/2020/03/coronavirus-stimulus-how-to-get-unemployment-aid-for-freelancer-contractor-part-time-workers-typically-left-out.html

- https://labor.ny.gov/ui/cares-act.shtm

- Dan LaRosa, Ritholtz Wealth Management

- https://studentaid.gov/announcements-events/coronavirus#zero-interest-questions>

- https://www.wilx.com/content/news/Some-mixed-status-families-wont-receive-stimulus-check–569798941.html