Credit improvement is a key pillar of how smart employers think about financial health. Prime credit scores save workers money on interest payments and fees, enable them to qualify for higher credit limits, and access otherwise unavailable financial opportunities with far-reaching implications for workers and organizations alike: We offer 9 tactics your workers can use to strengthen their credit.

Financial wellness programs should account for credit improvement.

Credit improvement is a key pillar of how smart employers think about financial health, broadly, personally.

We know a higher credit score opens doors to better financial products and services.

We know employees with prime credit scores can save money on interest payments and fees, qualify for higher credit limits, and access premium credit cards with valuable rewards.

And we know these benefits can reduce employee stress and boost mental health, financial stability and opportunity.

This is good for employers and for our workers.

HR for small businesses take note: Earned-wage-access apps are loans, says Consumer Financial Protection Bureau

HR for small businesses take note: Earned-wage-access apps are loans, says the Consumer Financial Protection Bureau, in its effort to protect workers who are forced to turn to them to make it paycheck to paycheck.

Absent affordable credit made possible by good credit scores, millions of workers are forced to turn to expensive, “bad debt.”

Broadly, this is debt that they cannot pay back at an affordable cost or within a reasonable time frame like payday loans and the burgeoning business of earned-wage-access apps, which have been compared to payday loans.

In a rule proposed last week, CFPB says that apps that allow workers to access their paychecks in advance, often for a fee, are providing loans and are subject to the Truth in Lending Act, a 1968 law that requires lenders to disclose all loan costs and fees.

In research released with the proposed rule, CFPB estimates that in 2022, 7 million workers received $22 billion through apps that worked with their employers, and 3 million workers received $9.1 billion through direct-to-consumer apps.

Workers who use earned wage access or what CFPB calls earned wage products took out on average 27 of these loans a year, roughly one loan for every biweekly paycheck.

This plays out like a revolving credit card balance with fees that would equal an average Annual Percentage Rate (APR) of over 100%, an interest rate higher than the most expensive subprime credit card.

CFPB finds that “most workers paid at least one fee and nearly all workers opt to pay a fee for expedited access to their funds” and that “costs may accumulate for workers who are frequently paid by the hour, have liquidity constraints, and receive public benefits.”

The agency will take comments on the proposed interpretive rule until the end of August.

Is earned wage access a loan?

Is earned wage access a loan?

Per CFPB, you may submit comments, identified by Docket No. CFPB-2024-0032, by any of the following methods:

Federal eRulemaking Portal: https://www.regulations.gov. Follow the instructions for submitting comments.

Email: [email protected]. Include Docket No. CFPB-2024-0032 in the subject line of the message.

Mail/Hand Delivery/Courier: Comment Intake—2024 Paycheck Advance Interpretive Rule, c/o Legal Division Docket Manager, Consumer Financial Protection Bureau, 1700 G Street NW, Washington, DC 20552.

Note that because “paper mail in the Washington, DC area and at the CFPB is subject to delay, commenters are encouraged to submit comments electronically.”

Reduce employee financial stress

Employee financial stress is a significant burden for most workers, impacting their overall well-being and job performance. Poor credit can exacerbate financial anxiety, as workers struggle to secure necessary loans or face high-interest rates on existing debt.

Financial wellness programs that help employees improve their credit scores can alleviate some of this stress, promoting a healthier, more focused, and productive workforce.

Reduce cost of employment, improve employee retention

Financial wellness programs that account for credit improvement can reduce the cost of employment by addressing your workers’ number one stressor, money. Employees who are less stressed about their finances are more likely to be engaged and productive at work.

There’s more. Are you asking yourself how to improve employee retention? Workers who feel supported by their employers in achieving financial security are more likely to stay with an employer, long term. They’re less likely to be depressed.

In a scoping review of peer-reviewed literature on financial strain and depression published from inception through January 19, 2023, eighty-three percent of articles (n = 48) reported a significant, positive association between financial strain and depression:

“Successful interventions were tailored to participants, were group-based (e.g., they included family members or other job seekers), and occurred over multiple sessions…There is a consistent, positive association between financial strain and depression in the United States.”

Financial wellness programs that alleviate financial strain have a vital role to play, with effects that span workers and organizations.

Support retirement savings

Improving credit scores can indirectly benefit retirement savings. Employees with lower interest rates on their debts can allocate more of their income toward retirement savings. Financial wellness programs that educate workers on managing their credit effectively can help ensure they are better prepared for retirement.

Advance equity

Credit scores reflect and perpetuate broader socio-economic disparities. By focusing on credit improvement, employers can help address some of these inequities. Financial wellness programs can provide resources and support to those who may have been disproportionately affected by financial challenges, offering a pathway to improved financial health and opportunities. And that’s good for workers and for employers.

Build a culture of financial wellness for small businesses

Building a culture of financial wellness for small businesses means thinking holistically about credit’s role in the lives of workers.

Prime credit scores are a crucial aspect of financial wellness, unlocking opportunities otherwise inaccessible, with far-reaching implications for workers and organizations alike.

Financial wellness programs that prioritize credit improvement can enhance workers’ financial stability, reduce stress, improve job performance and retention.

With these facts in mind we offer 9 tactics your workers can use to strengthen their credit (the CFPB’s “Want credit to work for you?” is also a valuable resource for workers).

Sharing relevant information with your workers shows you care about their financial health, which delivers its own benefits.

Employees who strongly agree that their employer cares about their overall wellbeing are 69% less likely to actively search for a new job, 71% less likely to report experiencing a lot of burnout, and three times more likely to be engaged at work.

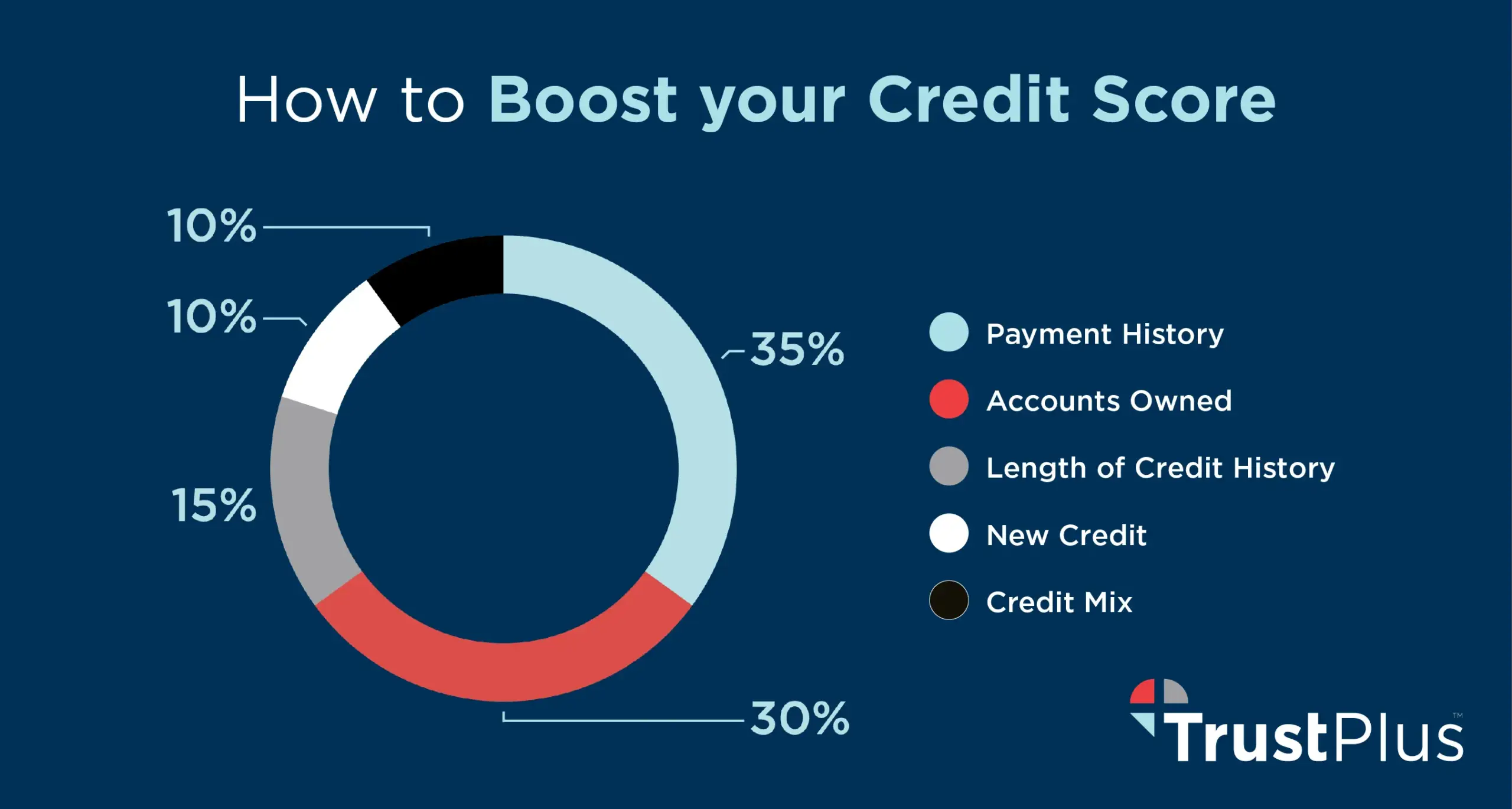

Boost your credit score with these 9 tactics:

- Check your credit report regularly: The first step to improving your credit score is to know where you stand. Obtain a free copy of your credit report from each of the three major credit bureaus—Equifax, Experian, and TransUnion—through AnnualCreditReport.com. Review your reports for errors or inaccuracies, such as incorrect personal information or fraudulent accounts, and dispute any discrepancies.

- Pay your bills on time: Timely bill payment is one of the most significant factors in determining your credit score. Set up reminders or automate payments to ensure you never miss a due date. Late payments can stay on your credit report for up to seven years, so it’s crucial to develop a habit of punctuality.

- Reduce your credit card balances: High credit card balances relative to your credit limit (also known as credit utilization) can negatively impact your score. Aim to keep your credit utilization ratio below 30%, and ideally below 10%, by paying down existing balances and avoiding high charges on your cards.

- Limit new credit inquiries: Each time you apply for credit, a hard inquiry is recorded on your credit report, which can temporarily lower your score. Avoid applying for unnecessary credit and only seek new credit when it is essential.

- Keep old accounts open: The length of your credit history contributes to your credit score. Closing old accounts can shorten your credit history and reduce your overall available credit, both of which can negatively affect your score. Keep older accounts open, especially if they have no annual fee, to maintain a longer credit history.

- Diversify your credit mix: Having a variety of credit types—such as credit cards, installment loans, and mortgages—can positively influence your credit score. However, don’t open new accounts solely for the sake of diversification; ensure you can manage additional credit responsibly.

- Negotiate with creditors: If you have a history of late payments, reach out to your creditors and ask if they can remove the negative marks from your credit report. Some creditors may be willing to make adjustments, especially if you have a good payment history otherwise.

- Consider a secure credit card: For individuals with poor or limited credit history, a secured credit card can be a helpful tool. Secured cards require a cash deposit as collateral, which serves as your credit limit. Using a secured card responsibly can help build or rebuild your credit over time.

- Become an authorized user: If you have a trusted family member or friend with a good credit history, ask if they can add you as an authorized user on their credit card. This can help improve your credit score by benefiting from their positive payment history and credit utilization.

Schedule a time with TrustPlus about your financial wellness programs, credit improvement, and capturing the benefits of a financially healthy workforce.